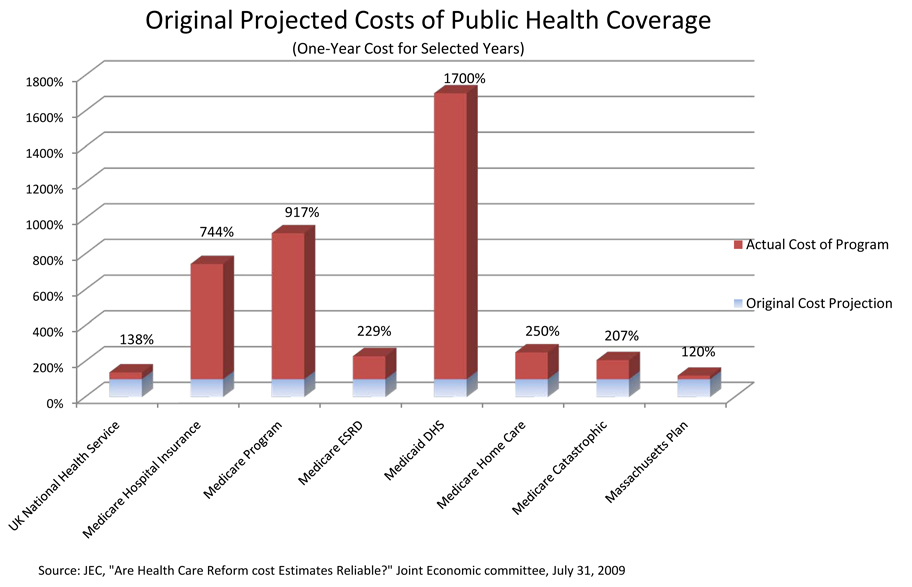

Last month, in a meeting at work, I listened to a presentation about medical billing and denials. During the presentation, the presenter made an offhand remark at insurance companies denying claims "without ever seeing the patient or knowing what the needs are". The unstated assumption was that a government run health plan would do a better job of making sure that people got the healthcare they need. (At my job, that's usually the assumption, stated or otherwise.)

But is that really true? Well, not if you hold up Medicare as an example of well-run government healthcare. This week, Scott Gottlieb wrote an interesting op-ed for the Wall Street Journal: "What's at Stake in the Medicare Showdown".

First, there's a mistaken belief that Medicare is better staffed than private plans, and can therefore make better decisions about patients' clinical circumstances and the access to new therapies they should have. Yet at any time, Medicare has about 20 doctors and 40 total clinicians (including nurses) inside the coverage office, and fewer than a dozen in the office that sets the rates that doctors are reimbursed for the care they provide. Private insurers employ thousands of doctors, nurses and pharmacists, many experts in new technologies.

Aetna has more than 140 physicians and about 3,300 nurses, pharmacists and other clinicians across its health plans. Wellpoint has 4,000 clinicians across its different businesses, including 125 doctors and 3,180 nurses. That works out to one clinician for every 9,000 people covered. United Healthcare employs about 600 doctors and 12,000 clinicians across all of its health plans and various health-care businesses.

Private plans use clinically trained people to establish access to new technologies and services, but they also consult with doctors on a case-by-case basis, determining whether a product or service should be covered. Competition for beneficiaries means private plans need to provide better access for appeals, modern services and more personal considerations than what's offered by Medicare, a monopoly supplier.

Recent data from Price Waterhouse Coopers found that private plans spend roughly four times more than Medicare on "consumer services, provider support, and marketing," which includes money spent answering the telephone to adjudicate individual issues. Smaller health plans use one clinician for every 10,000 beneficiaries. Medicare would need 4,500 clinicians to keep pace.

One place where the clinician disparity is most obvious is the delivery of cancer benefits. Medicare doesn't have a single oncologist on staff, yet since the year 2000 the program issued, by my count, 165 restrictions and directives on the use of cancer drugs and diagnostic tools.

A second common refrain is that Medicare is more efficient than private plans, spending less money per beneficiary to administer health services. But a lot of the money that private plans spend is on clinical specialists charged not only with reviewing individual cases, but also with ensuring that doctors and beneficiaries comply with plan contracts. Far from a selling point, not having these functions is one of Medicare's shortcomings.

Medicare doesn't need to hire doctors to weigh individual medical cases because it uses formulaic rules made in Washington to set broad and inflexible restrictions on medical practice. Nor does the program need to hire clinical staff to monitor compliance. It passes costs for that on to the broader health-care system by backing up its rules with the threat of costly civil and even criminal sanctions. Providers and medical product developers spend hundreds of millions of dollars on systems, personnel and paperwork to ensure compliance with Medicare's sticky morass of regulations - tasks made more expensive by the fuzziness of the program's regulations and the arbitrary way they are enforced.

When you put it that way, I'd far rather have my expenses reviewed by private insurance than by Medicare. Instead of an example to follow, Medicare looks like a cautionary tale of what not to do.

I work with a lot of bright people. I wish they would question their assumptions more often and not just fall back on the tired rhetoric of "profit-seeking companies are bad" and "government programs really do help people".